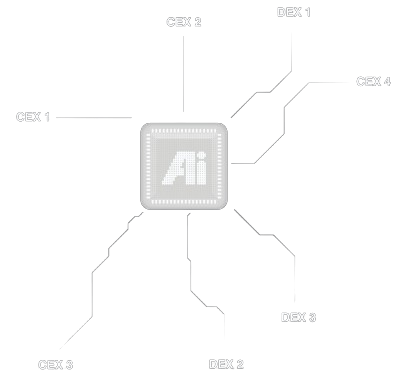

BS.AI®

OPTIONS

OPTIONSWe use Options to deliver powerful trading —but keep them under the hood to make it simple.

NOBEL PRIZE

NOBEL PRIZEWe use the Nobel Prize-winning Black-Scholes model to price derivatives — the same trusted method used by major investment banks worldwide.

AI-DRIVEN

AI-DRIVENOur very own AI continuously learns from on-chain activity and provides data to the model, enabling smarter pricing and risk management.

BS.AI acts as a Market Maker, dynamically pricing assets and eliminating the need for direct counterparty matching.

Flow: "Buyers ⇄ BS.AI® ⇄ Sellers"

- Simplicity

- Fair pricing

- High liquidity

We use Options to deliver powerful trading —but keep them under the hood to make it simple.

We use the Nobel Prize-winning Black-Scholes model to price derivatives — the same trusted method used by major investment banks worldwide.

Our very own AI continuously learns from on-chain activity and provides data to the model, enabling smarter pricing and risk management.

BS.AI acts as a Market Maker, dynamically pricing assets and eliminating the need for direct counterparty matching.

Flow: "Buyers ⇄ BS.AI® ⇄ Sellers"

- Simplicity

- Fair pricing

- High liquidity

Price engine

The price engine is comprised of these two components (volatility algorithm & Black–Scholes model) and when combined, they are used to calculate the value of each order reward on our exchange.

That's exactly what Brightpool delivers for exchanges, wallets, and trading platforms. We operate discreetly in the B2B space, letting real value shine bright on you. Ready to transform your platform?

Partner Benefits

- New Revenue Streams Unlocked

- Trading Reinvented For Users

- Zero Upfront Investment

- Zero Infrastructure Risk

Tap into options trading without building from scratch

White-labeled solutions - Customize the experience to fit your brand

Integrate our technology through simple APIs

We handle the complex backend systems

CEX CLIENT

- Issues time-limited orders (option-like contracts), locking assets (e.g., ETH) for the duration of the transaction.

- Receives a premium for each issued order, independent of the order execution outcome.

- Premium acts as an incentive to stimulate trading activity.

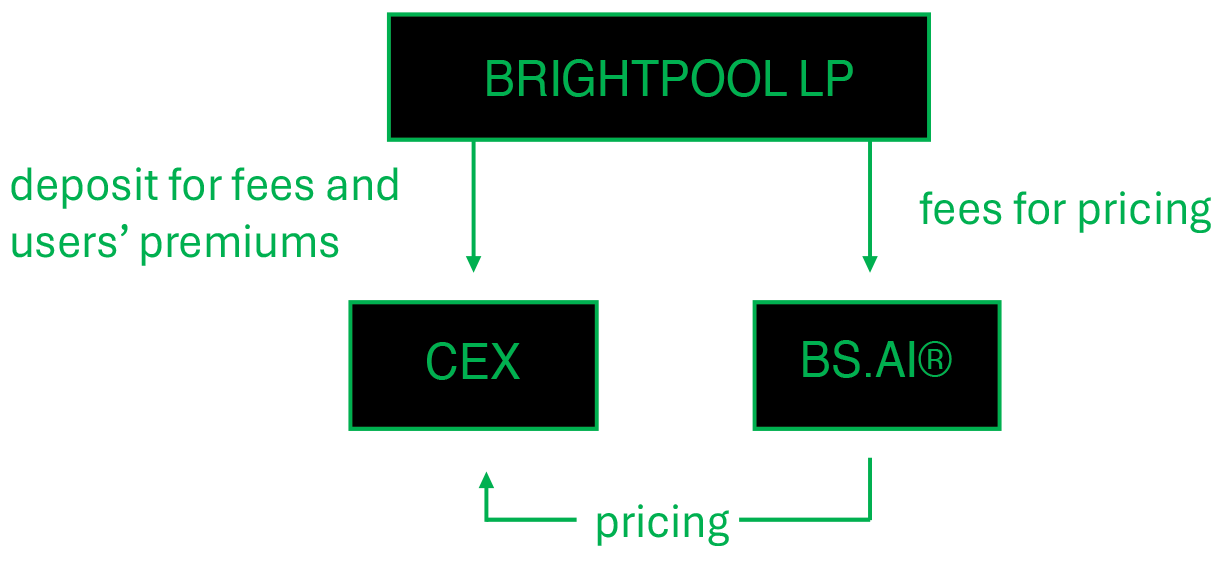

CEX(CENTRALIZED EXCHANGE)

- Facilitates a platform for clients to issue time-limited orders.

- Integrates dynamically generated pricing provided by the BS.AI module and presents it directly to users.

- Earns commissions (CEX fees) for every issued order, incentivizing transaction volume. Commissions are funded by the Brightpool Liquidity Pool.

BS.AI®(OPTIONS PRICING MODULE)

- Delivers real-time, dynamic order pricing to CEX via API, leveraging on-chain data.

- Employs an advanced Black-Scholes pricing model enhanced by AI algorithms for improved accuracy.

- Receives compensation from the Brightpool Liquidity Pool based on:SUBSCRIPTION FEESSUCCESS FEES

BRIGHTPOOLLIQUIDITY POOL

- Deposits funds directly into the CEX exchange accounts, utilized for: PREMIUM PAYOUTS TO CLIENTS ISSUING ORDERS and COMMISSIONS TO EXCHANGES (CEX FEES).

- Conducts regular (daily or weekly) cycles of replenishing or manually withdrawing surplus liquidity.

- Compensates the BS.AI module for pricing services.

- Generates profit from user-issued orders (options) expiring "in the money."